Introduction

For years, the dream of owning a house has been seen as the ultimate milestone of adulthood and financial success. But in today’s evolving financial landscape, many young earners and smart savers are asking a bold question:

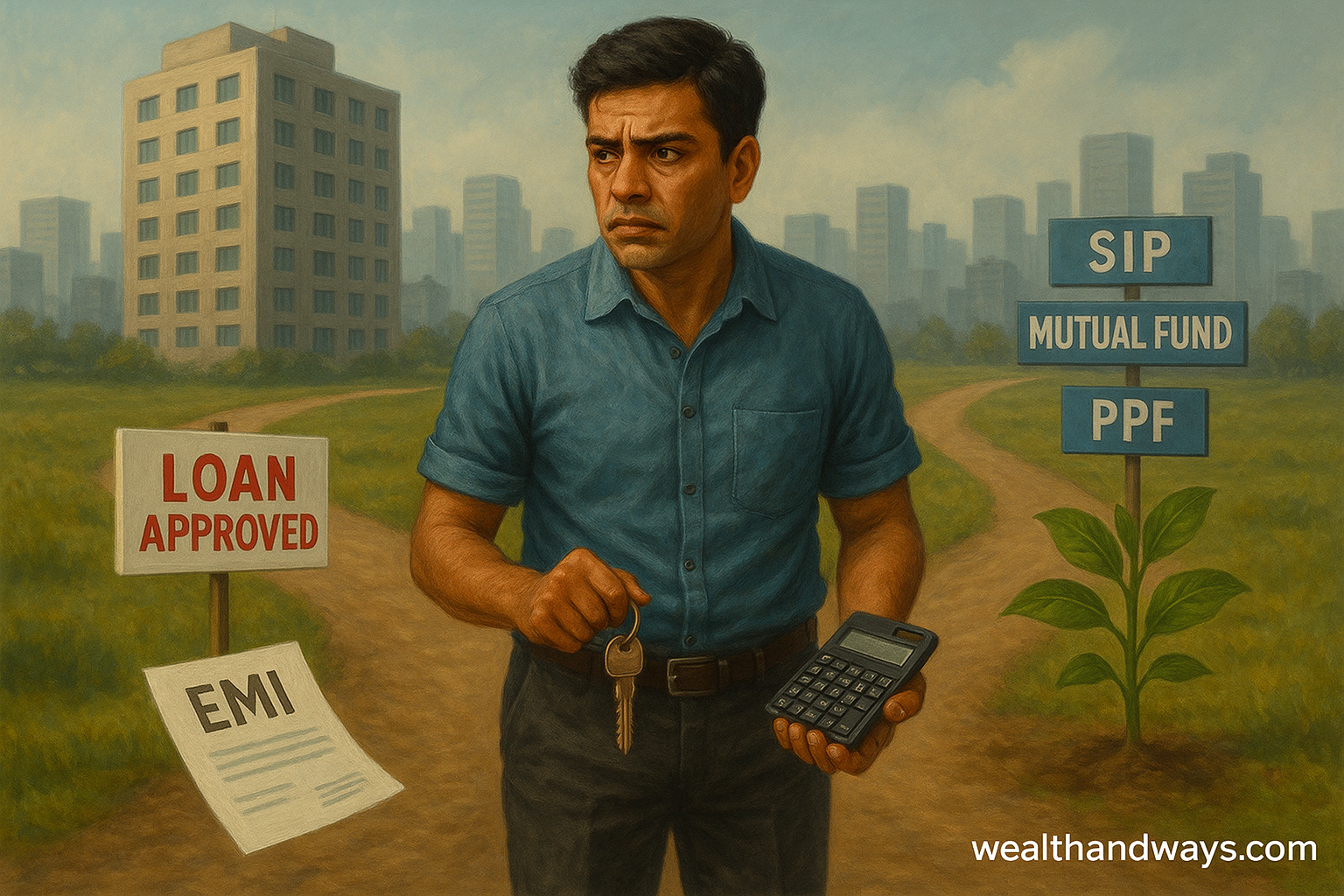

“Should I buy a house and commit to EMIs for 20 years, or should I invest that money and grow my wealth?”

Let’s explore both sides in plain language — and see which path might lead you to greater financial stability and freedom.

🏡 Option 1: Buying a House (and Paying EMIs)

Pros:

You own a physical asset

Security of having a roof over your head

Real estate generally appreciates over time

Emotional satisfaction of “owning your space”

Cons:

Long-term debt commitment (10–30 years)

High interest burden — you may pay 1.5x to 2x the house cost

Property taxes, maintenance, insurance, registration, repairs

Less liquidity — hard to sell quickly if you need money

💼 Option 2: Investing the EMI Amount (Instead of Buying)

Let’s say your home loan EMI is ₹30,000/month. If you invest that same amount into:

Mutual Funds (via SIP) with 12% annual average returns

PPF, ELSS, or index funds for long-term compounding

REITs or stocks to diversify your exposure

Over 15–20 years, your total investment could grow to ₹1.5 to 2.2 crores, depending on market performance and consistency.

Pros:

High liquidity (you can withdraw when needed)

Potential for greater returns than real estate

Lower stress (no debt)

More flexibility and mobility

Cons:

No fixed asset (house) to live in

Need discipline — no missed SIPs!

Market risk (but long-term investment smooths volatility)

📊 Let’s Compare

Criteria Buying a House Investing EMI Amount

Monthly Outflow Fixed EMI Flexible SIPs

Asset Type Real estate Financial assets (MF, PPF)

Liquidity Low High

Tax Benefits Yes (Sec 80C & 24b) Yes (ELSS, PPF, LTCG)

Flexibility Low High

Long-term Growth Moderate (6–8% avg) Higher (10–14% avg)

🔑 Final Thoughts

There’s no one-size-fits-all answer. If your priority is stability, owning a house may suit you. But if financial growth, flexibility, and freedom matter more, investing instead of committing to a home loan may lead to greater peace of mind — and a much stronger net worth.

📌 Smart takeaway:

You don’t always need to own a home to be financially secure. Sometimes, renting and investing wisely can get you further ahead — faster.

🚫 Disclaimer:

This blog is for informational purposes only. Please consult a licensed financial advisor before making major investment decisions.